₹1 crore — it sounds like a lot, doesn’t it?

That number has become the default benchmark in India’s term insurance market. You’ve seen it everywhere: ads, policy comparisons, even YouTube reviews. But here’s the real question…

Is ₹1 crore of term insurance actually enough to protect your family?

Or is it just a round number that sounds safe?

Let’s break it down.

Why Everyone Talks About ₹1 Crore

Over the past decade, life insurance companies have turned ₹1 crore into a buzzword — and for good reason. It’s easy to remember, sounds aspirational, and thanks to online term plans, it’s become surprisingly affordable.

If you’re under 35, non-smoker, and salaried — you could get ₹1 crore cover for ₹500–₹1,200/month depending on the policy term and tenure.

That’s helped boost awareness. But not everyone who buys ₹1 crore cover actually needs that amount — and many who need more settle for this as a default.

Does ₹1 Crore Actually Cover Your Family’s Needs?

To figure that out, ask yourself one thing:

How many years of income should my life insurance replace?

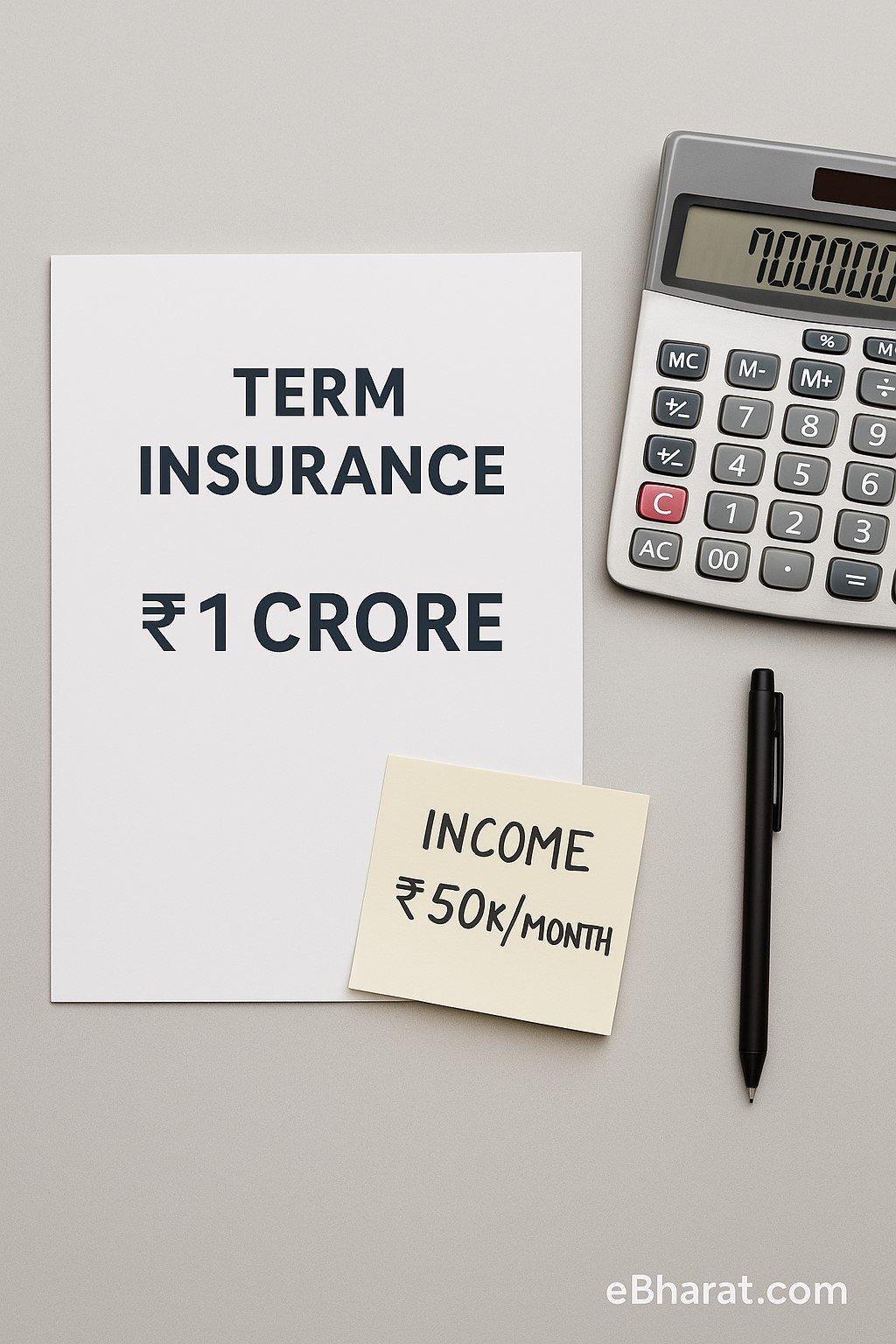

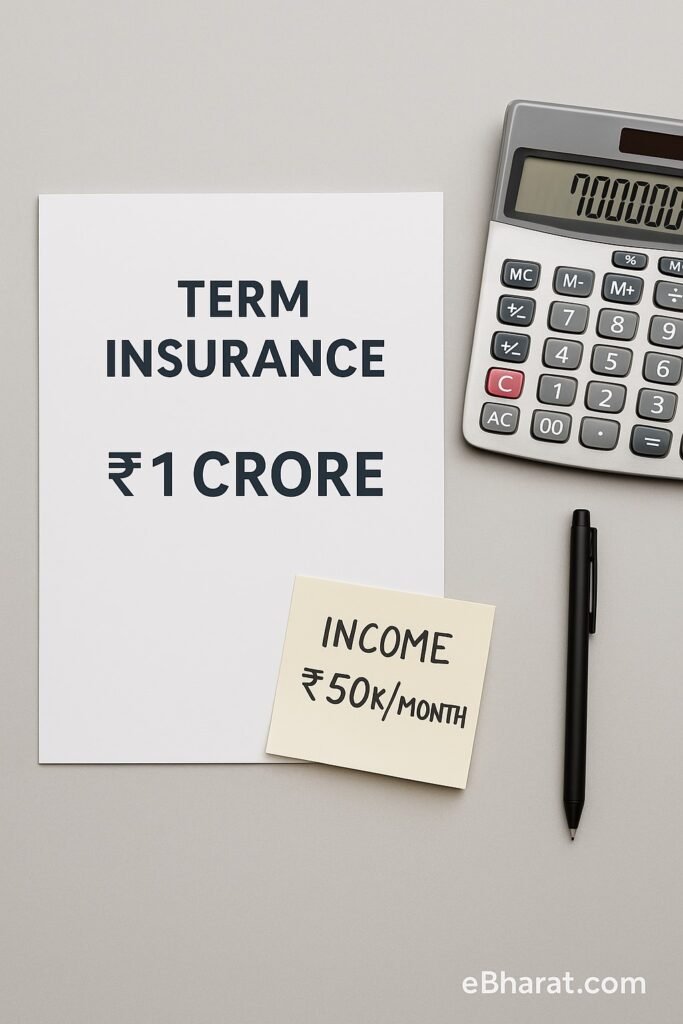

The general rule? 10 to 15 times your annual income.

Let’s do the math:

| Your Annual Income | Ideal Term Cover | Is ₹1 Cr Enough? |

|---|---|---|

| ₹3 – ₹4 lakh | ₹30 – ₹60 lakh | Yes |

| ₹6 – ₹8 lakh | ₹90 lakh – ₹1.2 Cr | Borderline |

| ₹10 lakh+ | ₹1.5 – ₹2 Cr+ | Likely not enough |

So if you earn ₹12 lakh/year, a ₹1 crore payout gives your family around 8 years of income — before accounting for inflation, EMIs, or education expenses. Not ideal.

Inflation Will Shrink That “Big” Number

Let’s say you’re 30 and buying a 30-year term plan.

By the time your family receives the payout (hopefully never), ₹1 crore in today’s money will be worth only ₹50–₹60 lakh — assuming average 6% inflation.

That’s a big drop. That’s why:

- Some insurers offer increasing cover options

- You can upgrade your policy during milestones (marriage, childbirth, etc.)

Smart tip? Start high when you’re young and healthy — premiums are lower, and your future is better protected.

Loans + Kids = More Cover Needed

If you’ve got:

- A home loan of ₹50–₹70 lakh

- Kids in private schools or planning abroad education

- Only one earning member in the household

Then ₹1 crore is likely not enough.

In these cases, aim for ₹1.5–₹2 crore or more, depending on your liabilities and savings.

But for someone who’s:

- Debt-free

- Has employer-provided cover

- No long-term financial dependents

… ₹1 crore could be more than enough.

When ₹1 Crore Might Actually Be Too Much

Rare, but possible. For example:

- You earn ₹15K–₹20K/month and live in a debt-free joint family

- You already have group cover through your job or government schemes like PMJJBY

- You don’t have long-term dependents

But here’s the thing — term insurance is so affordable that it’s better to slightly over-cover than under-cover.

Final Word: Don’t Follow the Crowd — Do the Math

₹1 crore is not a magic number.

It’s just a reference point.

Here’s what you should actually do:

- Use a trusted life cover calculator

- Factor in income, EMIs, dependents, and future expenses

- Always adjust for inflation

- Review every few years as your responsibilities grow

Because under-insuring your family can leave them vulnerable — and the difference is just a few hundred rupees a month.