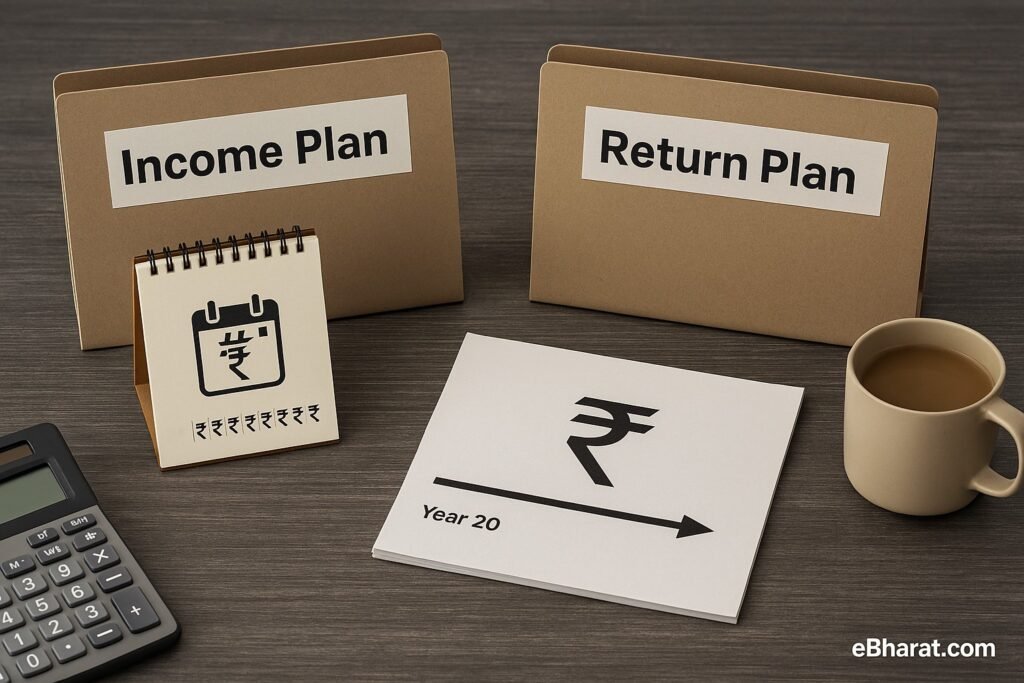

“Income Plan” or “Return Plan”?

If you’ve been exploring life insurance savings products, you’ve probably come across both these terms. And at first glance, they both sound like solid choices.

But don’t be fooled — while both offer guaranteed benefits, they’re designed for very different financial needs.

Let’s break it down in simple, everyday language so you can confidently pick the right one for your life goals.

What Is an Income Plan?

An Income Plan is like setting up a future salary for yourself.

Here’s how it works:

- You pay premiums for a few years (say 5–12 years)

- After a short waiting or deferment period, you begin receiving monthly or yearly payouts

- These payouts are guaranteed and continue for 20–30 years — or even for your lifetime (in some variants)

Example

You pay ₹1 lakh per year for 10 years.

After a 5-year deferment, you receive ₹25,000/month for 25 years.

That’s ₹75 lakhs in guaranteed income, plus a final bonus or maturity amount (if applicable).

Best For:

- People close to retirement

- Families who want predictable household cash flow

- Parents funding long-term goals (like college fees over many years)

- Anyone who wants regular, stress-free passive income

What Is a Return Plan?

A Return Plan is like a disciplined savings tool with a big payout at the end.

Here’s how it works:

- You pay premiums for a fixed term

- There’s no income during the policy term

- At maturity, you receive a lump sum payout — ideal for big financial goals

Example

You pay ₹1 lakh/year for 10 years.

At maturity (say, year 20), you receive ₹20–25 lakhs in one go.

Best For:

- Parents saving for a child’s education or wedding

- People planning a major expense like home buying

- Investors looking to create a long-term corpus

- Anyone who prefers lump sum wealth at a fixed date

Income vs Return: A Quick Comparison

| Aspect | Income Plan | Return Plan |

|---|---|---|

| Payout Style | Monthly / Annual Income | Lump Sum at Maturity |

| When You Get Paid | Starts after a few years, continues long-term | Only once, at the end of the policy |

| Best For | Cash flow during retirement or life goals | Funding major one-time expenses |

| Popular Example | HDFC Life Sanchay Plus – Income Option | HDFC Life Sanchay Plus – Guaranteed Maturity |

| Tax Status | Usually tax-free under Section 10(10D) | Same — if plan meets 10(10D) conditions |

So, Which One Should You Choose?

Ask yourself one simple question:

Do I want

Monthly income for peace of mind? → Go for an Income Plan

One big payout to fund a future goal? → Choose a Return Plan

But here’s a smart idea many financial advisors recommend:

Why Not Split the Difference?

If you have ₹2 lakhs/year to invest:

- Put ₹1 lakh into a guaranteed income stream

- Put ₹1 lakh into a lump sum return plan

This way, you get both steady cash flow + a big payout — covering short-term and long-term needs.

Final Word: Income or Return — What Really Matters?

There’s no one-size-fits-all solution. The best plan is the one that fits your life, your goals, and your peace of mind.

Some people need monthly stability. Others need wealth at a fixed future point.

Many families need both — and that’s okay too.

Whichever you choose, make sure:

- You understand the deferment and maturity timelines

- You know the Internal Rate of Return (IRR)

- You check that it qualifies for tax-free maturity under Section 10(10D)