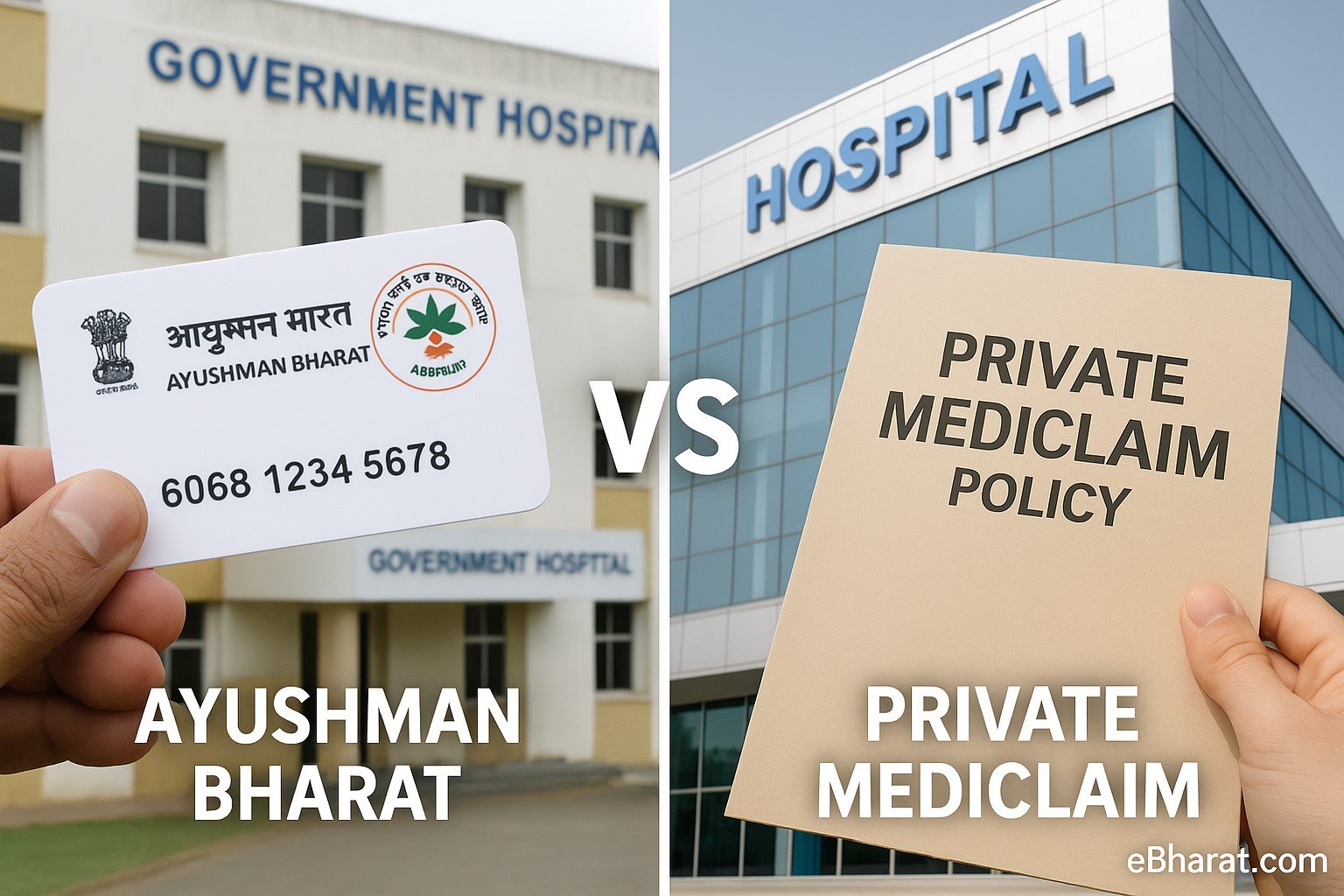

When it comes to health insurance in India, two options stand out for very different reasons — Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana (PM-JAY) and private mediclaim policies.

Ayushman Bharat, launched in 2018, is the world’s largest government-funded health scheme, offering free coverage for economically vulnerable families. Private mediclaim, on the other hand, is a paid health policy available to anyone who can afford the premium, with customizable features and higher sum assured options.

In 2025, with rising medical costs, understanding which works better for you (or if you should combine both) is crucial.

Quick Comparison Table – Ayushman Bharat vs Private Mediclaim

| Feature | Ayushman Bharat (PM-JAY) | Private Mediclaim |

|---|---|---|

| Coverage Amount | ₹5 lakh per family/year | ₹3 lakh to ₹1 crore+ |

| Eligibility | Low-income families listed in SECC data | Available to anyone who pays the premium |

| Premium | Free (paid by government) | Varies by sum assured, age, health |

| Hospital Network | Public + empanelled private hospitals | Private network + choice of premium hospitals |

| Pre/Post Hospitalization | Limited (3 days pre, 15 days post) | Comprehensive (30 days pre, 60–90 days post) |

| Additional Benefits | Basic secondary/tertiary care | OPD, maternity, critical illness, riders |

Strengths of Ayushman Bharat

- Free coverage for eligible low-income households.

- Wide reach across rural and urban areas.

- Covers major surgeries like cardiac, cancer, and kidney treatments.

Limitations of Ayushman Bharat

- Not available to everyone — eligibility is restricted.

- Lower flexibility in hospital choice compared to premium private plans.

- Limited coverage for OPD, medicines, and post-treatment care.

Strengths of Private Mediclaim

- Customizable coverage from ₹3 lakh to ₹1 crore+.

- Access to premium hospitals and advanced treatments.

- Add-ons for maternity, OPD, daily cash, critical illness, etc.

Limitations of Private Mediclaim

- Premiums increase with age and medical history.

- Exclusions in the first 1–4 years for pre-existing diseases.

Case Example

Shankar’s family in Rajasthan qualified for Ayushman Bharat, which covered his father’s ₹3 lakh heart surgery fully. However, when Shankar’s wife needed maternity care in a premium hospital, he relied on his private mediclaim policy for ₹5 lakh coverage. Together, both policies ensured zero out-of-pocket expense.

Why It Matters

Ayushman Bharat is a lifeline for low-income families, while private mediclaim offers flexibility and higher protection. If you can afford it, having both ensures broader and deeper health coverage.

Health cover is not one-size-fits-all. Share this eBharat.com guide so more families understand how to choose or combine Ayushman Bharat and private mediclaim wisely.

Internal Links:

- What to Check Before Buying Family Floater Health Insurance

- Tax Saving with Health Insurance – Don’t Miss These Sections

- 5 Tricks Health Insurance Agents Use – And How to Avoid Them