Mumbai | 10-Oct-2025, 09:30 IST — Filed on 10-Oct-2025, 08:45 IST via NSE/BSE Disclosure

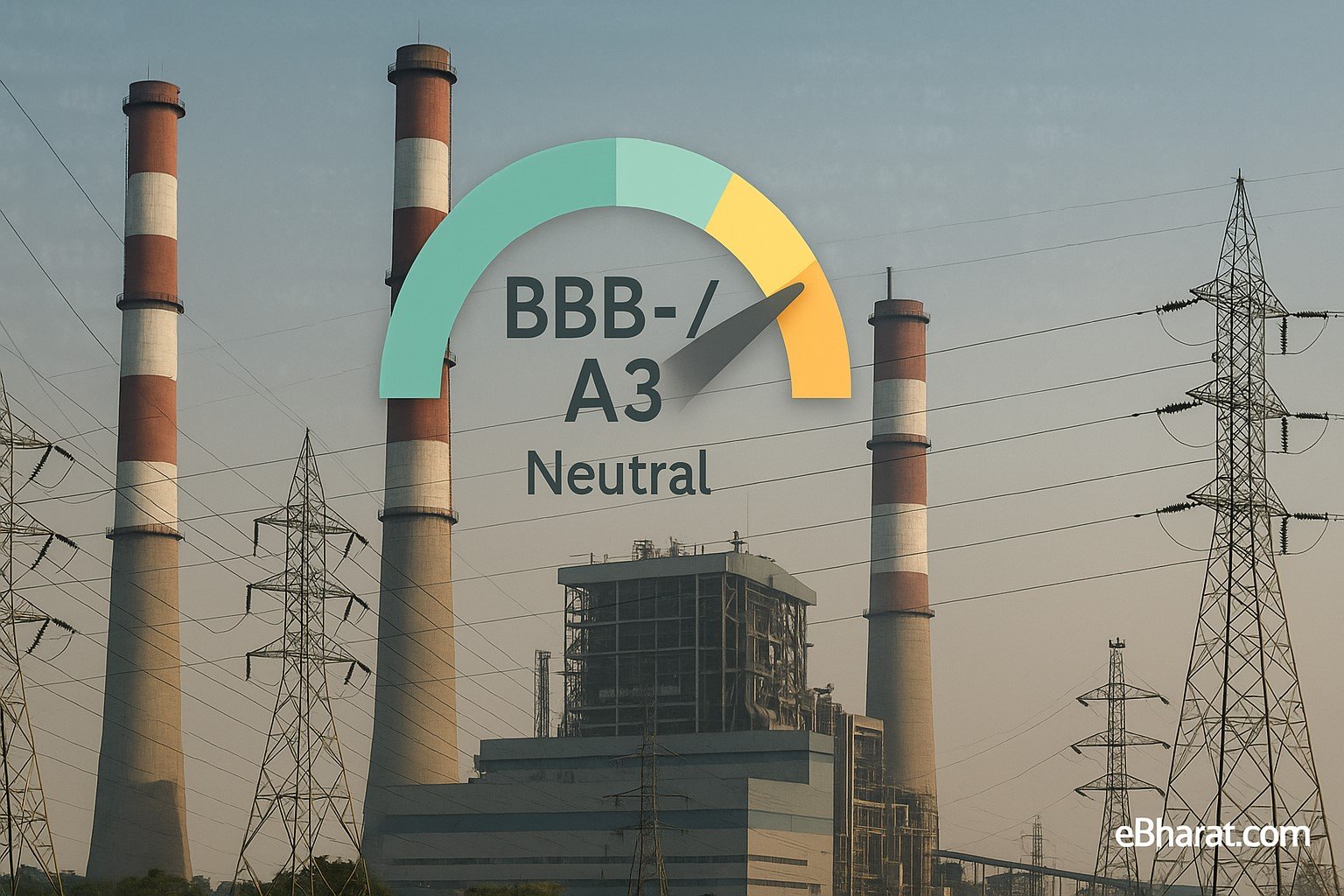

RattanIndia Power Ltd (NSE: RTNPOWER / BSE: 533122) has submitted a credit rating update to stock exchanges this morning, in line with SEBI’s disclosure requirements. The filing, made under Regulation 30 of the LODR, reflects the company’s ongoing engagement with rating agencies and compliance with continuous reporting norms.

Current Disclosure

- The company has notified exchanges of a rating update, though the filing did not immediately specify whether it represents an upgrade, downgrade, or reaffirmation.

- RattanIndia Power has historically been rated by CRISIL. As of May 2025, the agency had reaffirmed the company’s BBB- / Stable rating on its non-convertible debentures (NCDs) and A3 on its short-term bank facilities.

- At that time, CRISIL also withdrew its rating on ₹68.58 crore of long-term bank facilities, citing “no dues” confirmations from lenders.

Past Rating Profile

Looking back at recent rating actions gives context to today’s filing:

- May 2025: CRISIL reaffirmed BBB- / Stable (NCDs) and A3 (short-term facilities).

- 2024: Ratings held at the same level, though commentary flagged risks around litigation relating to Redeemable Preference Shares (RPS) with lenders such as REC.

- Drivers of stability: Long-term Power Purchase Agreements (PPAs) with Maharashtra State Electricity Distribution Company Ltd (MSEDCL), high plant availability, and timely payments have anchored the company’s profile.

- Risks noted: Dependence on coal supply, input cost volatility, and exposure to regulatory/counterparty delays.

Rating Drivers & Considerations

Analysts and investors will watch closely to see if the latest update signals:

- Upgrade Potential: Possible if leverage has improved further, with debt prepayment and higher cash balances.

- Reaffirmation: Likely if operational performance remains steady but risks (coal supply, litigation) persist.

- Downgrade Risks: Could arise if receivables stretch, fuel shortages impact PLF, or legal liabilities weigh on balance sheet strength.

Company Snapshot

- Business: Independent Power Producer with thermal power generation assets.

- Key Assets: 1,350 MW Amravati thermal plant in Maharashtra; Nashik plant under development.

- Promoters: Part of the RattanIndia Group led by Rajiv Rattan.

- Operations: Supplies power under long-term PPAs, primarily to MSEDCL.

Financial Performance (FY23–FY25):

- Revenue: ~₹3,600 crore (FY25) supported by long-term PPA offtake.

- EBITDA Margins: Stable at ~25–27%, driven by PPA-linked tariffs.

- Debt: Net secured fund-based debt reduced to ~₹188 crore as of FY25.

- Cash & Liquidity: Maintains trust and retention accounts (TRA) and cash reserves to cover near-term obligations.

Sector Context

India’s thermal power sector continues to face challenges:

- Fuel Supply: Availability of domestic coal is improving, but volatility and transportation bottlenecks persist.

- Policy Shifts: Rising renewable energy penetration puts long-term demand risks for thermal generators.

- Regulatory Scrutiny: Tariff disputes, PPA enforcement, and ESG-linked financing conditions weigh on outlook.

For RattanIndia, its long-term PPAs with MSEDCL remain the credit anchor, but sector headwinds highlight the importance of today’s rating update.

Ticker Snapshot — RattanIndia Power (NSE: RTNPOWER)

| Metric | Value |

|---|---|

| Price | ₹11.55 |

| Change | +0.43 (+3.87%) |

| 52-Week Range | ₹8.44 – ₹17.09 |

| Market Cap | ~₹6,200 crore |

Outlook

The rating update will provide investors clarity on whether RattanIndia Power’s credit profile is improving as debt reduces and PPAs continue to deliver stable cash flows.

- Positive scenario: An upgrade could lower borrowing costs, enhance investor sentiment, and open avenues for refinancing.

- Base case: A reaffirmation at BBB- / A3 keeps credit profile steady, signalling no new risks.

- Downside: A downgrade would raise financing costs and renew concerns over sectoral headwinds.

For now, the disclosure demonstrates regulatory compliance. The final rating rationale, once published, will determine the market’s response.