When Indians think of life insurance, two names come up again and again — Term Plans and Endowment Plans. Both promise financial security for your family, but they work in very different ways.

Many middle-class families still buy endowment plans thinking they are getting investment plus insurance, while younger buyers often insist on term plans as the only smart choice.

👉 The truth? Neither is “good” or “bad.” The right choice depends on your financial goals, income level, risk appetite, and savings discipline.

Quick Comparison Table

| Feature | Term Plan | Endowment Plan |

|---|---|---|

| Purpose | Pure protection for your family | Protection + savings/investment |

| Premium Cost | Low (high coverage for less money) | High (part of premium goes to savings) |

| Payout on Survival | None | Maturity benefit after policy term |

| Best For | Income replacement, large cover | Short/medium-term savings goals |

| Returns | No returns (only death benefit) | Low to moderate (4–6% typically) |

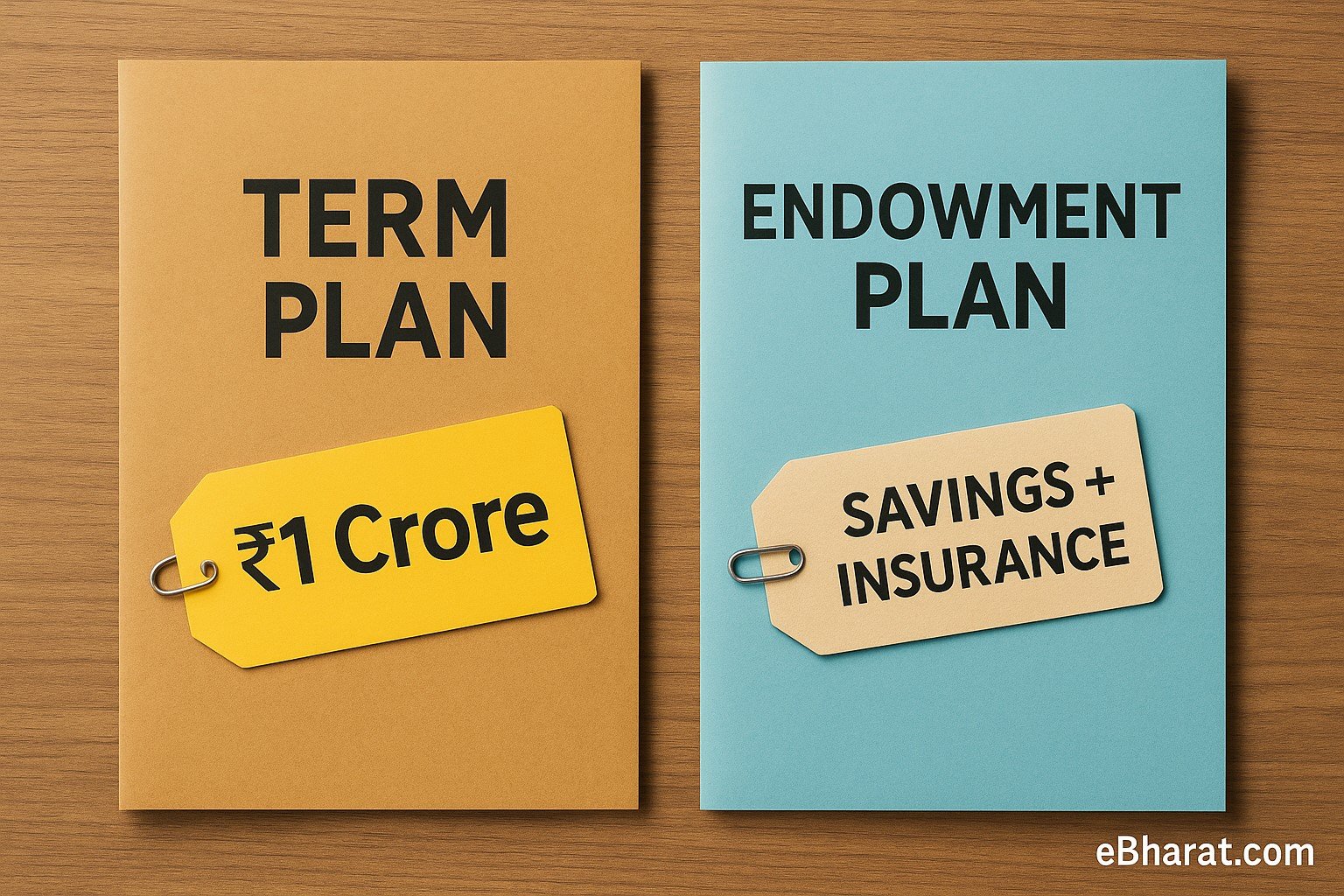

What Is a Term Plan?

A term plan is the purest form of life insurance. You pay a small premium for a large sum assured. If you survive the policy term, you don’t get anything back — but your family gets full protection if something happens to you.

👉 Example: A healthy 30-year-old can get ₹1 crore cover for just ~₹8,000/year.

Best for: People who want maximum coverage at lowest cost, and are disciplined enough to invest savings separately (in SIPs, PPF, etc.).

What Is an Endowment Plan?

An endowment plan combines insurance with savings. A part of your premium goes towards life cover, and the rest is invested by the insurer in safe instruments. If you survive the policy term, you receive a maturity amount plus bonuses.

👉 Example: For ₹10 lakh cover, the same 30-year-old may pay ₹50,000/year, and after 20 years, get back ₹12–14 lakh.

Best for: People who want a forced savings habit and guaranteed maturity, even if returns are modest.

When to Choose Which

- Choose Term Plan if: You want maximum coverage for minimal cost, and you’re disciplined enough to invest the difference elsewhere (like in mutual funds or PPF).

- Choose Endowment Plan if: You want a “forced savings” mechanism and guaranteed maturity value, even if returns are modest.

Case Example

Rohit, 35, compared both options:

- Endowment Plan: ₹10 lakh cover → premium ₹50,000/year.

- Term Plan: ₹1 crore cover → premium ₹10,000/year.

By choosing the term plan, Rohit saved ₹40,000/year. He invested this difference in mutual funds. After 20 years, his investments grew to ₹20 lakh, while the endowment plan’s maturity would have been only ~₹13 lakh.

👉 Lesson: Term + investment combo can create more wealth than an endowment.

Why It Matters

The biggest mistake is buying insurance without knowing the difference. Term plans protect first. Endowment plans save first.

In 2025, with rising costs and better investment options, choosing wisely ensures your family’s future stays secure.

Insurance should protect your life first — and investments should build wealth separately.

Related Reads on eBharat.com

- Should You Buy Term Insurance Without Medical Test?

- Which Life Insurance Plan Offers Highest Maturity Value in 2025

- 7 Mistakes Indians Make While Choosing Riders

🧐 Confused Between Term & Endowment?

Use Insurance+ to compare Term Plans vs Endowment Plans side by side. See premiums, coverage, and maturity values clearly before you decide.

👉 Compare Term vs Endowment on Insurance+