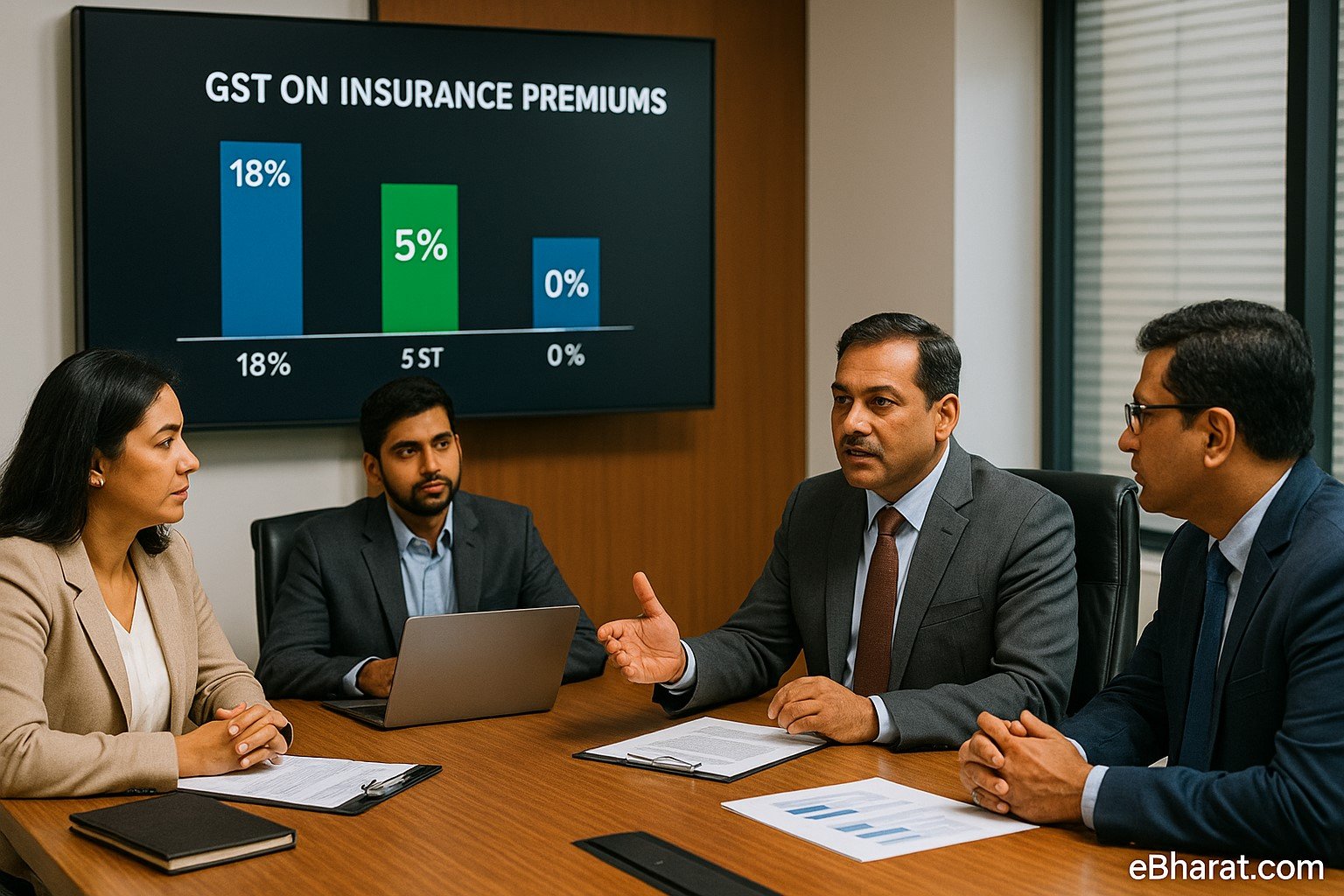

The debate over GST on insurance premiums is heating up. The government is considering removing the current 18% GST on premiums, which many consumers see as a welcome relief. However, surprisingly, the insurance industry itself is not asking for a 0% GST rate. Instead, insurers are lobbying for a reduced slab of 5% rather than a full exemption.

This perspective may sound unusual, but it comes down to how input tax credits (ITC) work in the insurance business.

Why Insurers Don’t Want a Full Exemption

Currently, insurers charge 18% GST on premiums and can claim input tax credits (ITC) on the GST they pay for business expenses like:

- Technology and IT services

- Marketing and advertising

- Distribution and agent commissions

If the government removes GST on premiums entirely:

- Insurers lose ITC benefits → They won’t be able to offset the GST they pay on their expenses.

- Operational costs will rise → Taxes on inputs like technology and marketing will become a cost burden.

- Consumer savings may shrink → Even though the headline GST rate is 0%, insurers might adjust base premiums upward to recover higher costs.

👉 This is why a 5% GST slab is considered a “middle path”—it reduces costs for policyholders while keeping ITC intact for insurers.

Industry Reactions

Executives in the sector have welcomed the government’s move but prefer a balanced approach.

A senior executive at a private life insurer explained:

“We welcome the government’s intent to make insurance more affordable. But a token GST, even at 5%, helps us maintain efficiency through input credits.”

Analysts also warn that moving straight to a zero-tax regime could create accounting distortions and disrupt insurers’ financial planning.

Related: Centre Considers GST Relief on Insurance Premiums Ahead of Diwali

Consumer Impact: 0% vs 5% GST

For policyholders, both options (0% GST or 5% GST) would reduce the burden significantly compared to the current 18%. The difference between 0% and 5% is not very large for families, but the 5% slab keeps the insurance ecosystem more stable.

| Premium (per year) | With 18% GST | With 5% GST | No GST |

|---|---|---|---|

| ₹10,000 | ₹11,800 | ₹10,500 | ₹10,000 |

| ₹25,000 | ₹29,500 | ₹26,250 | ₹25,000 |

| ₹50,000 | ₹59,000 | ₹52,500 | ₹50,000 |

Even with 5% GST, customers save substantially compared to the current 18% rate.

Policy Context

This debate comes just as the government is expected to announce GST relief for insurance premiums—possibly as a Diwali 2025 announcement.

For the insurance industry, the question is not only about tax relief but also about ensuring sustainability and operational efficiency.

Why It Matters

This issue is bigger than just tax rates. It’s about balancing affordability for families and stability for insurers.

- Consumers benefit from lower premiums.

- Insurers retain ITC, ensuring financial health.

- The insurance sector grows sustainably, making protection accessible for more households.

One thing is clear: Insurance is now being recognized as an essential service, not a luxury—and this shift will reshape India’s financial future.

Whether the government goes for 0% GST or 5% GST, both will reduce the cost of protection for Indian families. But insurers’ preference for a 5% slab shows that a balanced approach may be the best long-term solution.

📢 What do you think—0% GST or 5% GST? Which option makes more sense for India’s insurance sector? Share your thoughts with us on Facebook or Twitter.