Insurance Saves Tax — But That Shouldn’t Be the Only Reason You Buy It

Come January, and lakhs of Indians rush to buy insurance — not to protect their families, but to save a few thousand rupees in tax.

Sound familiar?

For many, insurance becomes a last-minute tax hack instead of a long-term financial shield. But here’s the truth:

Buying life insurance just to claim deductions under Section 80C is a mistake that could cost you in the long run.

Let’s break down the facts — and help you make smarter choices this tax season.

What Tax Benefits Does Insurance Offer?

Insurance does offer tax perks — and they can be substantial:

- Section 80C: You can claim up to ₹1.5 lakh per year for premiums paid on life insurance policies.

- Section 10(10D): Maturity benefits are tax-free if premiums are less than 10% of the sum assured.

- Section 80D: Separate deductions for health insurance premiums (₹25,000 to ₹1 lakh, depending on age).

But tax-saving should be a bonus — not the primary motivation.

Why Tax-Driven Insurance Buys Can Backfire

When you rush to buy a policy for tax-saving, you’re likely to fall into one of these traps:

1. Low Returns

Endowment and money-back plans — often marketed as “safe savings” — typically offer returns of just 4%–5%, barely keeping up with inflation.

2. Long Lock-in Periods

Most traditional plans require a 10–20 year commitment. Exit early, and you lose money to surrender charges.

3. Inadequate Life Cover

Tax-saving plans often give you ₹2–₹5 lakh in cover — which is nowhere close to the ₹50 lakh–₹1 crore protection your family may actually need.

4. Wrong Fit for Your Life Stage

A single, one-size-fits-all plan bought in haste rarely matches your changing needs over time.

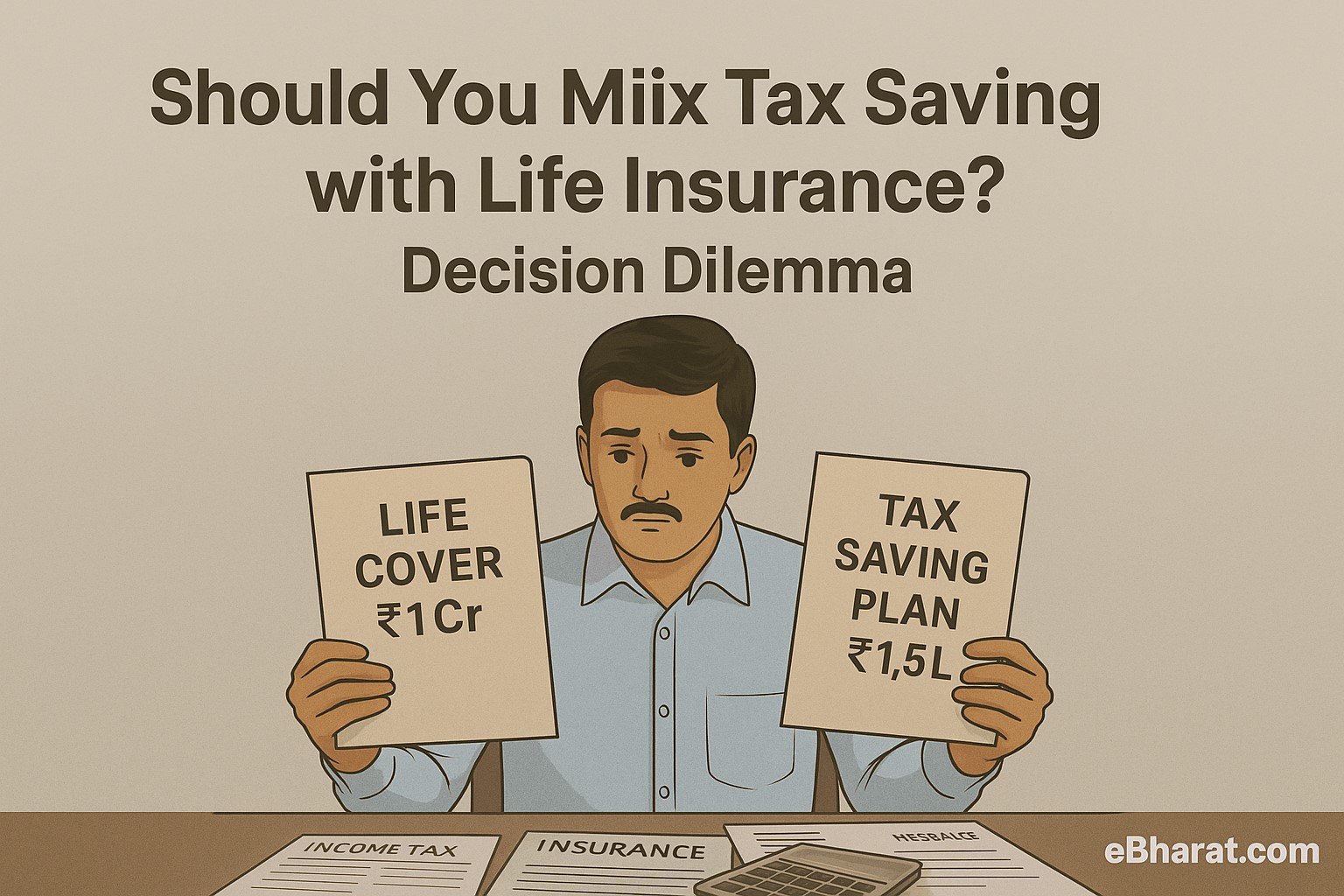

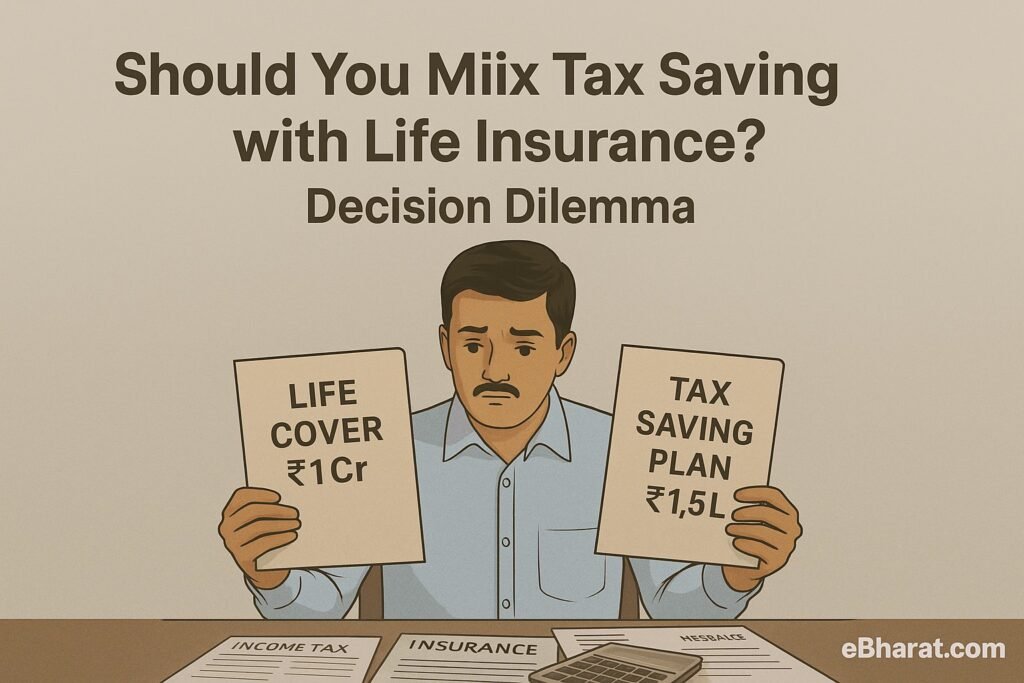

So while you might save ₹40,000 in taxes, you could lose much more in missed returns or insufficient coverage.

A Smarter Approach: Separate Protection from Investment

If you really want to build a strong financial foundation and save tax, here’s what works:

Use Term Insurance for Life Protection

It offers high cover (₹1 crore or more) at low premiums — ideal for securing your family.

Use ELSS, PPF, or NPS for Tax-Saving & Growth

These offer better liquidity, higher returns, and still qualify for Section 80C deductions.

Plan Early in the Financial Year

When you wait till March, you panic-buy. Start in April, and you can choose calmly and wisely.

Review Before You Commit

Ask if the plan meets your family’s real needs — not just your CA’s checklist.

What Happens When You Mix Up Tax and Insurance?

Let’s say:

- You earn ₹7 lakh/year

- You buy a traditional life policy with ₹1.5 lakh annual premium

- It promises ₹15 lakh over 20 years

But here’s what goes wrong:

- Your life cover is way too low for your family’s needs

- You’re locked in for 20 years — even if your priorities change

- Your actual returns (post-inflation) may be as low as 2%–3%

What’s a better move?

- ₹10,000/year term plan with ₹1 crore cover

- ₹1.4 lakh invested in ELSS or NPS

Now you have:

- Real protection

- Tax savings

- Potential for 10%–12% returns

Should You Buy Insurance to Save Tax?

Yes — but only if the policy makes sense for your life.

A well-chosen insurance policy can protect your loved ones and offer tax benefits. But if you’re buying a plan that doesn’t suit your goals just to fill up a deduction column, you’re likely wasting money.

Final Word: Let Insurance Do Its Real Job

Insurance is not a tax product. It’s a promise.

A promise to protect your family when life takes an unexpected turn.

Before you sign that policy form in March, ask yourself:

- Does this plan actually protect my family?

- Will I stick with this for 10, 15, or 20 years?

- Does it align with my financial goals?

If not, it’s time to rethink.

Because peace of mind is worth more than a ₹45,000 tax break.